Foreign suppliers looking to import goods into the European Union (EU) are subject to import duty based on a number of factors. One of the factors that affects the duty to be paid is the value of the goods to be imported. This article explains how to determine value of the goods declared and how customers use CAPLINQ’s fiscal representation service to reduce their import duties by reducing the value of goods being imported into the EU.

How do EU customs determine the value of goods?

There are two ways that the EU customs office determine the value of goods at the time of import into the EU

- The Customs Tariff Number used at the time of import

- The value of the goods declared by the importer at time of entry

What is the Customs Tariff Number

The Customs Tariff Number, also called the Tariff Code, Harmonization Code or HS Code is a European standardized 10-digit code used to classify traded products. Each and every traded product imaginable can be classified by a tariff number. These tariff numbers are separated into 21 sections (at this writing) that identify the broad category of the product. Each section then splits further into chapters which then narrows down right to the exact product being imported.

For example, the Tariff Number 3907.30.00.90 refers to Epoxide resins; in primary forms. This is the tariff number used by the Epoxy Molding Compounds that CAPLINQ manufactures and sells.

Every European customs office refers to a multilingual database called TARIC (TARif Intégré de la Communauté) (French: Integrated Tariff of the European Community) that contains all of these tariff numbers, and along with them, there is a recorded history of all the importers that have ever imported products into the European Union using this tariff number. Naturally, with all this history is also the value of the goods that was declared at the time of import. These two elements — Customs Tariff Number and “Value of Goods declared” — provide a very good indication of what the value of the goods are when they arrive at customs. The list of tariff numbers is open to the public, but it is likely no coincidence that the value of the goods recorded at the time of entry is not publicly available.

What are the “Value of the Goods Declared?”

The second way the EU uses to determine the value of the goods is the “Value of the Goods Declared” by the importer at the time of entry. This second method is beautiful in its simplicity, but this is where many importers end up “over reporting” and end up paying more than they need to in import duties. It is always requested to supply a commercial invoice at the time of import. In the absence of any other information, importers often report the “Customers Sales Price” to customs.

Regardless of the “Value of the Goods Declared” provided, the customs officers will check this declared value against the history of prices reported for this tariff number. If the value is higher than the recorded history, the customs officer will accept your declared value and impose duty based on this value. If it is much lower, the importer will get a notice to please recheck the value of the goods declared. Notice that they never come back to you to inform you that the value of the goods is higher than other importers!

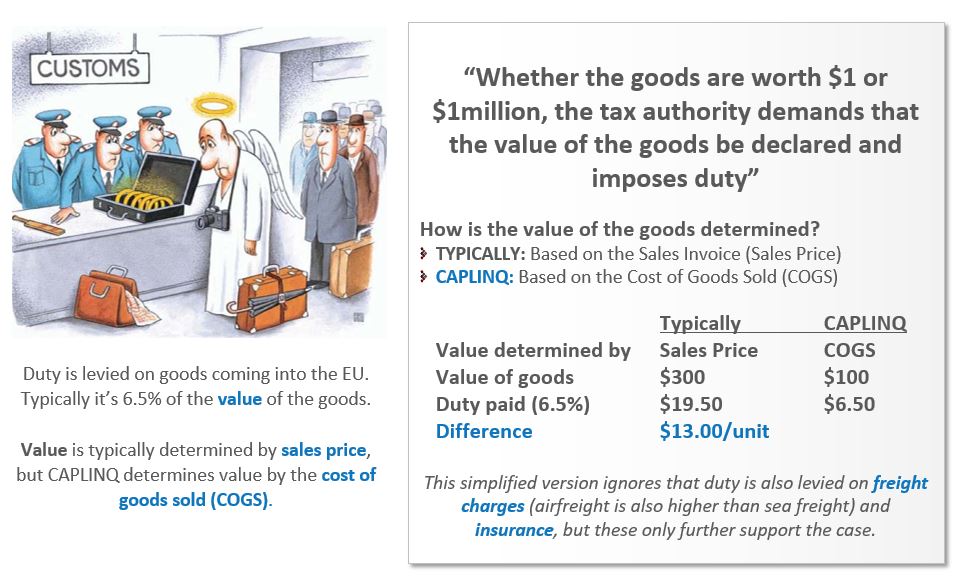

Whether the goods are worth $1 or $1 million, the customs officer demands that the value of the goods be declared and imposes a duty rate. It is in the best interest of the importer (and their customers) to have this value be as low as possible to minimum the duty paid.

CAPLINQ’s Fiscal Representation Service saves money by selecting the best Tariff Number

In another article, we explain how the import duty due is calculated. One of the elements is the choice of Tariff Number. Each Tariff Number may have different import duty rates that are imposed on it. The import duty rates can range from 0% up to some very high percentage depending on many factors concerning that particular traded good. For example, if the product is badly needed, or the technology cannot be obtained within the EU, the duties are low or 0%. On the other hand, if the that particular traded product is protected within the EU such as sugar or dairy products, then the tariff rates can be very high. These rules can change often, so it’s important to check the latest regulations concerning that particular traded good.

The specific tariff code can be selected differently, if we can convincingly argue that the traded good in question belongs in a more favorable tariff number. For example, using our example above of Epoxy Molding Compounds, a halogen-free epoxide can have a more favorable tariff number than a halogen-containing epoxide. During our fiscal representative setup phase, we look into what the most favorable tariff number is for the traded product and recommend it for use.

CAPLINQ’s Fiscal Representation Service saves money by reducing the value of goods declared

Most foreign suppliers with EU customers don’t realize that import and sales of traded goods are actually two separate transactions. Yes, the goods must be imported into the EU before they can be sold, but the first transaction is recorded as an import transaction and the second as a sales transaction.

This is important to note because importers are often worried if that if they use a lower value for the import value than they do for the sales transaction then they might get into trouble with their customers. For example, if customers were to learn that the sales value is 3–8 times the import value (which is often the case), then they might get offended and demand a price decrease. As your fiscal representative, CAPLINQ signs a Non-Disclosure Agreement (NDA) that ensures that customers never see the import value.

As your fiscal representative, CAPLINQ signs a Non-Disclosure Agreement (NDA) that ensures that customers never see the import value.

Once foreign suppliers recognize this, they often ask “how low can we (legally) go to reduce import duties”? CAPLINQ’s recommendation is the Cost of Goods Sold (COGS) price.

The COGS price, also referred to as the production value or the carrying value is the cost of products manufactured by the importer. This definition is sometimes subjective for companies looking to reduce their tax burden, but for our purposes, it is very specific — namely all the costs related to the production of the good including:

- The parts, raw materials and supplies used (often called the Bill of Materials or BOM Costs)

- All labor costs to produce the material or parts, including payroll taxes and benefits

- Business overhead allocated to production

*Note this does not include any sales, marketing or manager administration charges

Is declaring the COGS price as the Value of the Goods Declared” legal?

This question comes up often as companies want to save money, but of course want do not want to do anything illegal. Let’s start by understanding that you, as the importer, know more about your own product and its production process than any customs officer. At the same time, the custom officer (through forms and documents) is only ever asking you a simple question, “Can you please tell me the value of your product?”

In this simple question, there is an unasked question: “To whom?”. Importers are being asked to declare the value of their goods without being specifically asked to declare to whom this value applies. The real question that should be asked is “What is this value of these goods to you?”

The real question that should be on the customs declarations forms is not “What is the value of the goods?” but “What is the value of the goods to you the importer?

Asked in this way, the value is no longer the sales price to the customer, but the replacement cost of the product to the importer. To help importers with this question, we often ask them this same question a different way, “If you were to lose these goods at the border, how much insurance money would you require to cover your losses?” Asked this way, importers often look inward at exactly the elements that make up the COGS price: BOM cost, labor rates and associated overhead.

So who is the importer of record for import

Here we come to the second important element of why we can use the COGS price at the time of import. If you are selling your products directly to your customer on an EX WORKS basis, then your customer becomes the importer, and the question of “What is the value of the goods to you?” is different. In this case, the value of the goods IS the sales price and not the COGS price.

By appointing CAPLINQ as your fiscal representative, CAPLINQ acts on behalf of the foreign supplier, which means that the foreign supplier is the owner of the goods and therefore is also the importer of record. CAPLINQ simply handles the transaction as your fiscal representative.

Multinationals have long known the secrets of customs valuations and COGS pricing

Fiscal representation and importing against the COGS price is well-known by multinationals. For multinationals that have sales offices in Germany, France, the Netherlands or any other EU country, they are used to importing the goods using the COGS price and then selling to their customers at a higher sales price.

Imagine this scenario: A multinational has a widget that costs $10 to make in their factory in Japan (or the United States, China, Canada or any other country outside the EU) and imports goods into the EU to sell to customers for $30. They have done this for many years and then decide to sell their Japanese factory to a group of investors that do not have a sales office in the EU. Is it fair that the same widget, made in the same factory coming to the EU all of a sudden has duty imposed on it at $30 instead of $10? Of course it’s not, and it’s exactly the logic we use when discussing with customs officers who agree with us entirely.

What risks are involved in importing goods at the COGS price?

None. Foreign suppliers are often worried that importing goods at the COGS price carries a risk to it — but it is completely unfounded. CAPLINQ has a fiscal representation license that allows us to import goods into the EU. Companies that are granted this license (including CAPLINQ) often have to go through a full financial audit to be sure that the company is not invoiced in any illegal activities including fraud or money laundering.

Furthermore the tax authorities, once they grant this license to fiscal representatives, require them to make a significant deposit with the tax authorities to ensure that if there are any significant concerns, that there are funds they can withhold until the matter is resolved. CAPLINQ of course has such a deposit with the tax authorities.

A simplified example to illustrate the CAPLINQ advantage

The following example illustrates what CAPLINQ’s fiscal representation service can do for you and your EU customers.

Assume the following to be true:

- Product Description: Epoxy Molding Compound

- Product Tariff Code:: 3907.30.00.00

- Duty Rate: 6.5%

- COGS Price: $100

- Sales Price: $300

As you can see, on a single product, CAPLINQ’s fiscal representation service could save you and/or your customer $13.00 in duty charges.

CAPLINQ can often make the goods available to your customers in Europe for less than they pay in duty charges alone

Please visit www.caplinq.com to learn more how CAPLINQ’s fiscal representation service is used as part of our order fulfillment services. You can also contact us to find out more about how to reduce your EU import duties by paying duty on the production value (COGS) instead of the sales price.

Thank you President Trump. MAGA!